European Freight Rates Face Immediate Corrections on Soaring Diesel Prices

Market Monday - Week 12 – Assessing the crisis impact on full truck load rates

Two weeks ago, we warned that the de facto blockade of the Strait of Hormuz could shatter the balance of the European diesel market, and unfortunately, the “prolonged blockade” scenario we modeled is becoming our new reality. The sudden loss of a significant share of global oil supply has pushed crude prices past the $ 100-per-barrel threshold, triggering historic, asymmetric retail diesel price spikes across Europe.

The effects of this macroeconomic shock have hit European pumps with unprecedented velocity, heavily assisted by multiplying factors of national excise and tax structures. Below is a breakdown of the relative and absolute commercial diesel price changes across key European markets between Weeks 9 and 11:

The reason for large variance in diesel price developments across the major European countries partially lies in differences in local policies.

Germany, France, Denmark, and Sweden have rejected immediate fuel-price shields or direct tank rebates, prioritizing budget conservation and instead relying on antitrust authorities to monitor retail price hikes. The Spanish, Italian, and Austrian governments have expressed a more cautious approach and are considering tax-cut measures, but have implemented none yet.

Other countries are using a combination of direct regulation of prices or profit margins for the fuel market (Belgium, Slovenia, Croatia) or indirect influence, like Poland and Hungary in their approach of mitigating retail cost increases via state-controlled market entities.

The differences in policies sparked intense cross-border “fuel tourism”, particularly from German commercial operators to Poland seeking to capture arbitrage savings of up to €0.50-0.60 per liter, which is draining Western Poland’s supply hubs.

The Romanian government extended a specific, targeted support scheme that provides a direct financial grant of RON 0.85 per liter of diesel exclusively for registered road transport and distribution operators.

Variances in measurement lead us to a more fragmented and dynamic European market, where fuel prices, rules, and policies change overnight. To understand the true cost effects, we mapped these macro price surges directly onto operational logistics. Leveraging the Transporeon TCO (Total Cost of Ownership) Model, we analyzed how the recent spikes alter the fundamental economics for three specific European lanes:

Poland to Germany (Poznan to Essen): On this roughly 765 km route, the extreme fuel price surges in Germany and Poland have pushed the calculated fuel share of total costs from 24.6% up to 28.4% and drove a 5.3% increase in total operating costs. The baseline rate calculation now requires an absolute increase of ca. €62 per trip to compensate for the increase in fuel costs.

Spain to Netherlands (Zaragoza to Rotterdam): Covering over 1,515 km, the calculated fuel’s share of operating costs on this lane has jumped from 25.3% to 28.1%, translating to a 3.9% rise in total costs. Consequently, the February benchmark rate needs a ~€72 upward total correction.

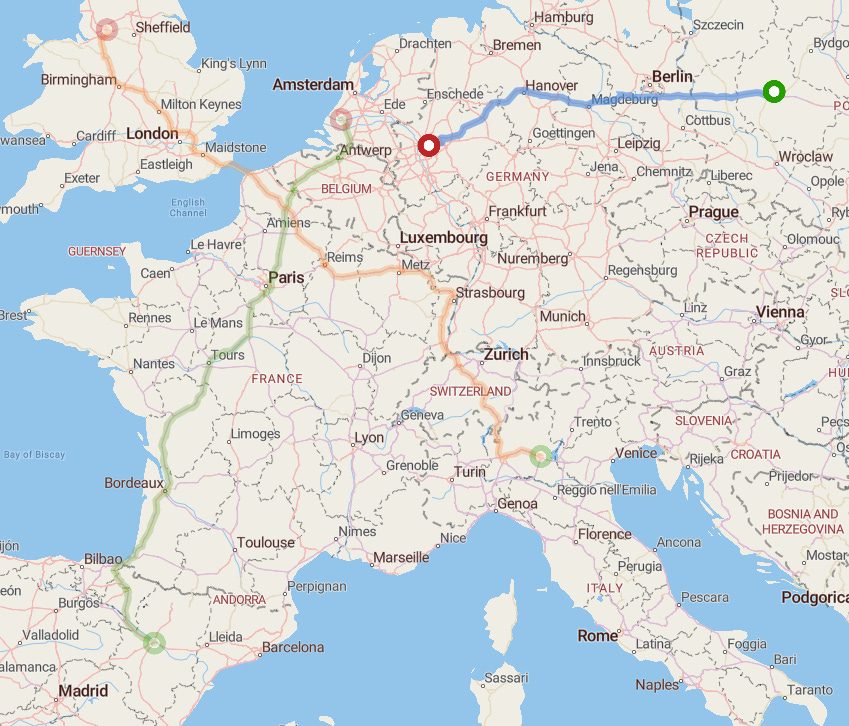

Italy to United Kingdom (Brescia to Manchester): Despite being the longest lane in our sample at nearly 1,680 km, the milder localized fuel surges resulted in a smaller relative shift: calculated fuel share increased from 23.4% to 25.1%, causing only a 2.3% total cost bump. Applied to a higher base rate, this dictates an ~€84 absolute rate increase.

These figures highlight how rapidly geopolitical shocks can change lane-level costs. As fuel policies and pump prices literally change overnight, we are utilizing our TCO algorithms across shipper networks to cut through the noise. In such a dynamic market, having an objective, data-driven baseline is the only way to determine which rate adjustments are genuinely fair for all parties involved, instead of applying one-size-fits-all solutions.

Oleksandr Kulish

Senior Consultant