Greening the Roads: Toll Updates in Europe

European toll systems are undergoing significant changes, driven by the imperative to cut CO2 emissions in line with the Paris Agreement.

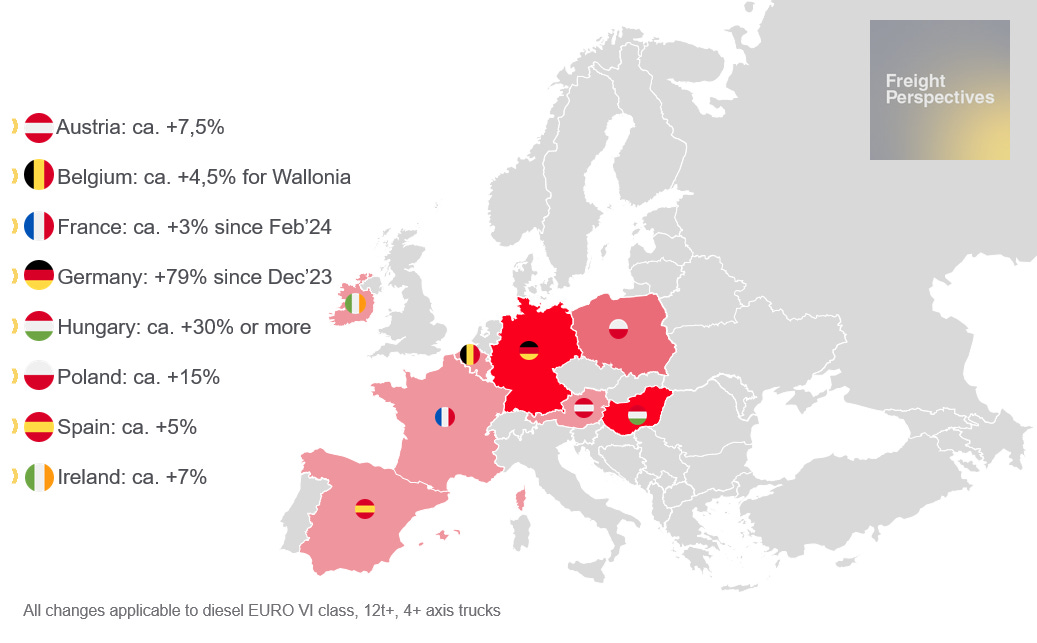

Here is an overview of current toll increases:

Map of significant changes in toll rates across Europe

Germany has increased tolls by around 30%, incorporating a 200-euro charge per tonne of CO2 emitted. Austria is implementing toll changes from January 2024, considering factors like distance, axle configuration, Euro emission class, and CO2 performance. Hungary has also adjusted tolls, factoring in frequency of use, CO2 emissions, and external costs, resulting in a 30% average increase.

Looking ahead, Denmark is set to introduce a new truck toll from January 2025, focusing on emissions and kilometers traveled. These changes aim to make transport greener, with Denmark targeting a CO2 reduction of 0.3 million tonnes by 2025 and 0.4 million tonnes by 2030.

Spain, however, is further exploring alternatives to tolls, considering rail freight transport and potential CO2 taxes from 2027.

The shift puts pressure on trucking companies to reduce emissions and encourages manufacturers to develop technology aligning with sustainability goals.

The Effects of Increased Toll Rates

The recent changes to the German toll structure, implemented on December 1, are already demonstrating a significant impact. Traditionally accounting for approximately 11% of the average full truckload cost, this percentage is projected to rise to around 18%.

An analysis of transportation rates, based on data collected from 55 shippers, indicates an average overall increase of 6.5% for domestic German full truckload costs. With already narrow operating margins, carriers will be unable to absorb this additional expense and will seek to pass it on to shippers. Latest data on Transporeon Market Insights confirms this and shows already a 5.9% increase in contracted rates within Germany from week 48 (Nov. 2023) to week 6 (Feb. 2024).

The projected 6.5% apply to linehaul costs and do not include any pre and post-carriage. Tolls also apply to re-positioning and empty mileage, which will put pressure on carriers to pass these costs along as well. The success of compensation negotiations will be uncertain and delicate. To mitigate the impact, carriers must strategically plan their routes and continuously optimize fleet utilization to alleviate the toll burden.

Currently, there is no indication that the mounting cost pressures on carriers will ease any time soon. If demand increases in 2024, it is expected that both spot and contract rates will also rise. Conversely, if current capacity levels persist alongside weak demand, any rate increases are likely to be minimal.

Future data will reveal the extent to which tolls affect rate levels and provide insights into whether the toll adjustments will significantly influence pricing dynamics in the European transportation industry.